Gross margin is one of the most scrutinized metrics on a company’s financial statements—and for good reason. It reflects how efficiently a business delivers its product or service, and plays a critical role in shaping valuation, investor confidence, and operational planning.

But behind every gross margin number lies a fundamental question: What should we include in Cost of Goods Sold (COGS), and are we modeling COGS in a way that reflects the actual economics of the business?

At Attivo, we view COGS and gross margin as more than accounting categories. They are strategic levers—tools that enable executive teams to validate growth plans, pressure-test scale assumptions, and build investor-ready narratives.

Translating Business Mechanics into Financial Models

At its core, COGS captures the costs required to deliver and support a product or service for customers. COGS does not include the cost to acquire the customer. Accurately modeling COGS begins with a deep understanding of how the product is delivered and supported, including which teams are involved, what infrastructure and platforms are required, and how those components scale.

For SaaS and AI companies, costs typically include:

- Customer support teams providing ongoing support

- Cloud compute and hosting supporting the production environment

- Machine learning inference costs

- Software tools required to manage and operate the platform

- Merchant processing fees and third-party delivery tools

- Implementation teams responsible for onboarding new customers

In AI-driven businesses, this becomes especially nuanced. Model inference costs, GPU-intensive real-time processing, and high-frequency data transactions can drive significant expense. If development environments (used for model training or QA) are not clearly segregated from production infrastructure, the gross margin will become distorted, and create confusion around a key valuation driver.

For product-based companies, COGS includes:

- Inventory and bill of materials (BOM)

- Warehousing, shipping, and fulfillment logistics

- Labor for production, quality control, and customer support

- Amortization of capital equipment and facilities (if they are used to support revenue)

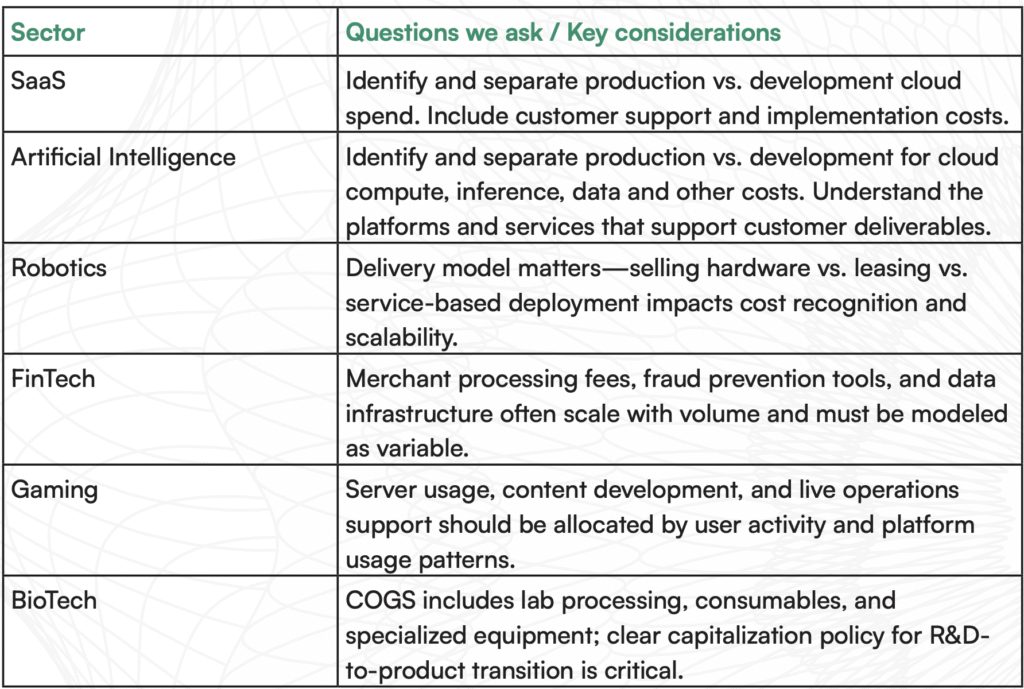

How COGS Works In Different Sectors

COGS is not a one-size-fits-all concept. While the core principle—capturing the cost of delivering your product or service—remains the same, its application varies significantly across different business models. Delivery model, infrastructure, regulatory considerations, and product lifecycle all shape what gets classified as COGS.

Understanding these structural differences is essential for building a credible margin story. When finance teams misclassify spend or overlook sector-specific nuances, gross margin benchmarks become unreliable, and scale assumptions break down. The table below outlines common COGS drivers and modeling considerations across five sectors Attivo frequently works with. Each requires a distinct approach to cost allocation, forecasting, and investor communication.

COGS Modeling as a Tool for Scale and Credibility

Early-stage teams often default to overly broad classifications—e.g., treating all cloud spend as OPEX. That may work in the earliest stages, but it rarely holds up under scale or investor scrutiny. Gross margin is not just a financial output—it is a signal to investors about scalability, capital efficiency, and valuation potential and therefore it is important COGS are correctly identified and accounted for as such.

In SaaS, the medium gross margin is 73%, while the top-performing quartile is 89% based on Attivo’s internal benchmarking data. For product companies, margins closer to 50% are more common, shaped by logistics and manufacturing efficiency. In AI, benchmarks are still evolving, and investors are developing assumptions and models.. In all cases, margin performance directly influences fundraising outcomes and perceived scalability.

That is why we model COGS from the bottom up, asking:

- What activities are required to deliver the product or service?

- Which teams, systems, or vendors are involved?

- Are the costs fixed and/or do they scale with revenue, headcount, or other metrics?

This operational lens surfaces gaps. In one robotics engagement, a client’s financial model initially assumed a one-to-one support ratio: one person for every deployed robot. That worked during the initial learning phase, but when modeled across hundreds of units, the cost structure broke down. The model exposed a key misalignment between delivery design and growth.

That insight triggered a strategic pivot: the company invested in backend engineering to build monitoring tools, reducing the need for human support requirements. What began as a gross margin analysis became a catalyst for product and delivery redesign.

Accurate COGS modeling is more than a reporting exercise—it’s proof of scalability. Accurately accounting for COGS separates costs that grow with revenue from those that don’t, clarifies levers around pricing, infrastructure, and service delivery that protect gross margin, and gives investors confidence in the growth story.

Want to sharpen your COGS model or align your margin strategy with investor expectations? Contact the Attivo FP&A team to learn how we can help.